Ever wondered why the yield on your crypto deposits changes every few hours? Unlike a traditional bank where a manager or a central bank decides your savings rate, Interest Rate Models is an algorithmic framework in decentralized finance that automatically sets borrowing and lending rates based on supply and demand. These models ensure that a protocol doesn't run out of money while still giving lenders a fair return. If you've used a platform like Aave or Compound, you've already interacted with these invisible mathematical engines.

The Secret Sauce: Utilization Rate

To understand how rates move, you first have to understand the Utilization Rate is the ratio of the total assets currently borrowed to the total assets available in the lending pool . Think of it as a measure of how "busy" the pool is. If a pool has 100 USDC and users have borrowed 80, the utilization is 80%.

Why does this matter? Because if utilization hits 100%, lenders can't withdraw their money. That's a nightmare scenario for any DeFi protocol. To prevent this, models use the utilization rate as the primary trigger to move interest rates up or down. When demand for loans spikes, the rate climbs to discourage more borrowing and attract more lenders.

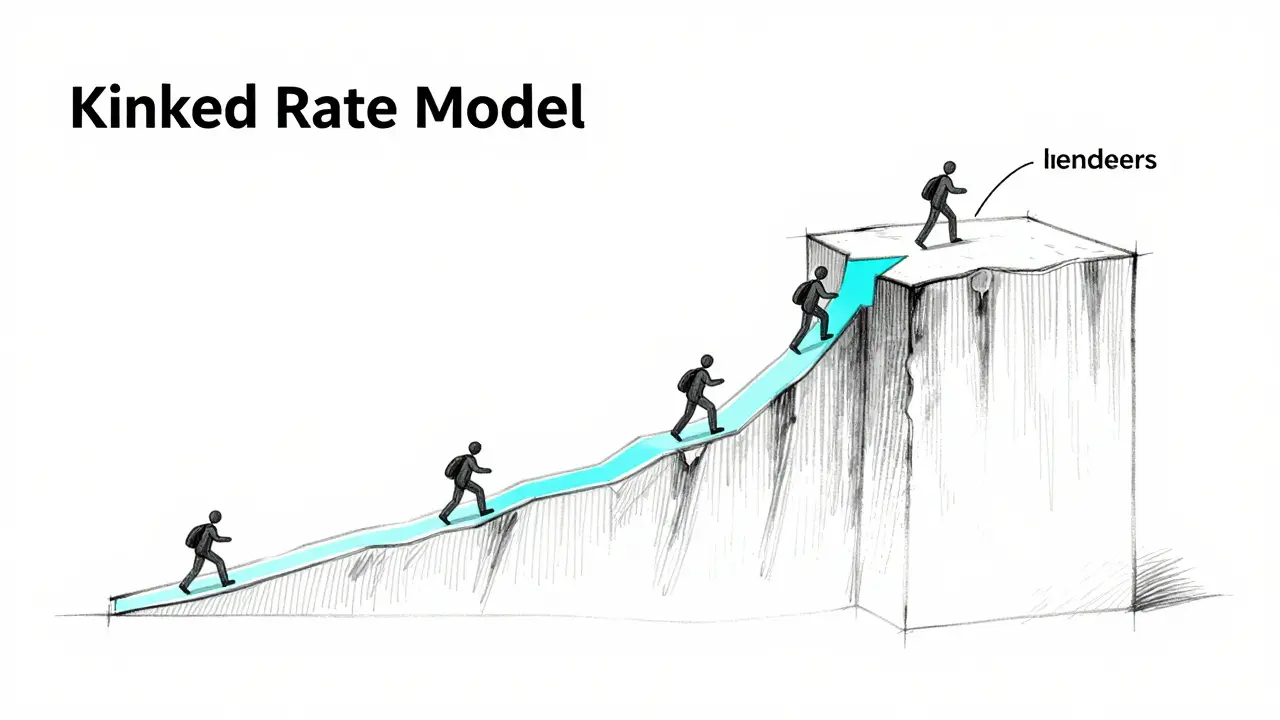

Linear vs. Kinked Rate Models

Not all protocols calculate rates the same way. Most fall into two main camps: linear and kinked. A linear model is simple-as utilization goes up, the rate goes up at a steady pace. But this can be risky because rates might not rise fast enough to stop a liquidity crunch.

Enter the Kinked Interest Rate Model is a piecewise linear function where the interest rate slope increases sharply after a specific utilization threshold, known as the kink . This is the gold standard for major platforms. Imagine a hill that is gentle for a while and then suddenly becomes a steep cliff. That "cliff" (the kink) is usually set around 80-95% utilization. Once the pool hits that point, the borrow rate skyrockets. This does two things: it forces borrowers to pay back their loans and makes it incredibly attractive for new lenders to deposit funds.

| Protocol | Typical LTV Ratio | Rate Model Type | Key Attribute |

|---|---|---|---|

| Aave | Up to 80% | Kinked (Piecewise) | High liquidity, stable/variable options |

| Compound | Up to 75% | Kinked (Dynamic) | Conservative, high technical clarity |

| MakerDAO | 66% - 75% | DSR Based | Conservative vault-based system |

How Different Protocols Play the Game

Different platforms have different philosophies. Aave is the giant of the space, often dominating about 35% of the total value locked (TVL). They use a sophisticated kinked model that lets them offer both stable and variable rates. For example, while USDC supply APYs might average around 7.47%, the borrow rate is usually slightly higher-around 8.94%-to cover the protocol's spread.

Compound takes a slightly different approach. They focus on a tight set of collateral assets like ETH and WBTC. Their borrowing APY for USDC has hovered around 4.10% in recent stable periods, making it a go-to for users who want more predictable costs. Meanwhile, MakerDAO doesn't act like a typical pool; it uses a Daily Savings Rate (DSR) which has recently seen peaks around 11.5%, fundamentally changing how users mint DAI.

The Risks: Volatility and Liquidations

It sounds perfect on paper, but algorithmic rates have a dark side: volatility. During a market crash, everyone wants to pay back their loans or withdraw their collateral at once. This can cause the utilization rate to swing wildly. If it pushes past the kink point, borrow rates can spike to 50% or even 100% APY in minutes.

This is where the "Health Factor" comes in. If the interest you owe grows too fast because of a rate spike, your loan-to-value (LTV) ratio worsens. If your health factor drops below 1, the protocol triggers a liquidation. Your collateral is sold off to ensure the lenders get paid back. It's a brutal but necessary mechanism to keep the system solvent.

Pro Strategies for Navigating Rates

Experienced DeFi users don't just deposit and forget; they play the rates. This is often called "rate arbitrage." If Aave is offering 8% on USDC but Compound is only paying 4%, a user might move their liquidity to Aave to capture the higher yield.

However, if you're doing this, keep an eye on the gas fees. During network congestion, a single transaction can cost $50 to $200. If you're moving $1,000 to chase a 2% difference, you'll actually lose money in the short term. The rule of thumb is to only rotate capital when the expected gain outweighs the transaction cost over at least a 30-day window.

The Future: AI and Smoothing

We're moving past simple linear formulas. The next generation of DeFi is focusing on "rate smoothing." Aave V4, expected around Q2 2025, aims to reduce those violent spikes around the kink point so users aren't blindsided by sudden costs.

Beyond that, 2026 is looking like the year of AI integration. We're seeing protocols experiment with machine learning to predict utilization trends before they happen, adjusting the kink point dynamically instead of relying on a static governance vote. This could mean more stability and better capital efficiency for everyone.

What happens if utilization hits 100%?

If utilization hits 100%, it means every single cent in the pool has been borrowed. Lenders cannot withdraw their funds until borrowers repay their loans. To prevent this, DeFi protocols use "kinked" rates that make borrowing incredibly expensive as utilization approaches 100%, incentivizing borrowers to pay back and lenders to deposit more.

Why are DeFi rates more volatile than bank rates?

Traditional banks set rates based on central bank policies and quarterly reviews. DeFi rates are algorithmic and updated in real-time based on every single deposit and loan. This transparency allows for efficiency but means any sudden shift in market demand is immediately reflected in the interest rate.

Is a high LTV ratio dangerous?

Yes. A high Loan-to-Value (LTV) ratio means you have borrowed a large amount relative to your collateral. If the price of your collateral drops or the interest rate spikes (increasing your debt), you are much more likely to hit a health factor below 1 and face liquidation.

What is the difference between APY and APR in DeFi?

APR (Annual Percentage Rate) is the simple interest rate without compounding. APY (Annual Percentage Yield) includes the effect of compounding your interest over time. In DeFi, most supply rates are shown as APY because interest is often added to your balance continuously.

Can I predict when interest rates will change?

While you can't predict the future, you can watch the utilization rate on the protocol's dashboard. If utilization is creeping up toward the "kink" point (usually around 80-90%), you can expect a sharp increase in borrowing costs very soon.

Suvoranjan Mukherjee

8 April, 2026 . 16:25 PM

Great breakdown of the mechanics! Just to add some alpha, most users forget that the effective yield is often skewed by incentive programs or liquidity mining rewards which can make a "low" base rate actually more profitable than a high one if the token emissions are strong. Keep grinding! 🚀

Bruce Micciulla Agency

10 April, 2026 . 09:25 AM

the math here is basic at best and honestly ignoring the systemic risk of recursive borrowing where people loop their collateral to inflate yields which just creates a house of cards waiting for a single oracle failure to wipe everything out because these kinked models dont account for the velocity of a panic sell off in a truly illiquid environment where you cant even find a buyer for the collateral

Arlen Medina

12 April, 2026 . 04:26 AM

Finally someone explains it simply! US-based protocols are absolutely crushing the game right now and it's exactly why we're the leaders in the space. Don't let the offshore stuff fool you, the real liquidity is here!

Susan Wright

12 April, 2026 . 15:23 PM

Keep in mind that gas fees on Ethereum can totally eat your profit if you're just moving small amounts. I always suggest checking L2 options like Arbitrum or Optimism if you want to actually play the rate arbitrage game without getting wrecked by the network.

Adriana Gurau

13 April, 2026 . 23:38 PM

Imagine thinking a basic table of LTV ratios is "insightful" 🙄. It's all so elementary that it's almost quaint. I've been analyzing liquidity pools since the early days of Uniswap and this is just... basic. 💅

david head

14 April, 2026 . 00:32 AM

this is super helpful thanks 💎🙌

Robert Coskrey

15 April, 2026 . 16:57 PM

I concur with the author's assessment of the risk associated with high LTV ratios; it is an imperative consideration for any serious investor...

June Coleman

16 April, 2026 . 06:01 AM

Oh look, another guide telling us to put money into algorithmic black boxes and hope for the best. I'm sure it's all totally safe and definitely not a way to lose your life savings in ten minutes. 🙄

vijendra pal

17 April, 2026 . 21:51 PM

bro the AI part is gonna be insane!! 🤖 we wont even need to check dashboards anymore just let the bot do the swapz and make bank 💸💸💸

JERRY ORTEGA

19 April, 2026 . 07:12 AM

just a heads up for the newcomers if you're staring at that health factor and it's getting close to 1.1 just add more collateral man dont risk the liquidators taking a cut of your bag its not worth the stress

Sonya Bowen

20 April, 2026 . 07:45 AM

Consider the ethical dimension of algorithmic liquidation. It's a cold mechanism that prioritizes protocol solvency over human stability.

shubhu patel

21 April, 2026 . 08:02 AM

I really appreciate how this post explains the difference between linear and kinked models because it can be quite confusing for someone who isn't deeply immersed in the technical side of things and I think it's important to have these resources available for everyone regardless of their experience level.

Nicholas Whooley

21 April, 2026 . 16:02 PM

It is heartening to see such a comprehensive guide. I believe this will empower many new users to navigate the DeFi landscape with greater confidence and security.

Emily 2231

21 April, 2026 . 16:56 PM

The implementation of these algorithms is a front for central bank surveillance. They want us in these pools so they can track every move we make while pretending it is decentralized. THE STATE IS ALWAYS WATCHING

Joshua Aldrich

22 April, 2026 . 13:04 PM

honestly i think the real issue is the oracle delay... if the price feed lagg by even a few seconds during a flash crash the whole kinked model doesnt matter coz you're already liquidted b4 you can top up your collateral. just happened to me on a smaller pool last year and its a nightmare

alex rodea

23 April, 2026 . 11:11 AM

Keep it up! You've got this!

Lauren Gilbert

24 April, 2026 . 07:56 AM

There is something poetic about the way these rates fluctuate like a digital tide, reflecting the collective anxiety and greed of thousands of anonymous users all interacting with a piece of code that doesn't care about them. It makes me wonder if we are creating a new kind of financial nature that we can't actually control.

Carmelita Gonzales

25 April, 2026 . 16:07 PM

it is a lot to take in but very useful for anyone trying to understand where their money goes in these pools